Simulating an economy with a Repuation System

This study aims to investigates the economic impact of reputation mechanisms in a decentralized market with adaptive agents. In the literature review for this study, the simulation is considered within the broader literature on online marketplaces, virtual economies, and reputation systems. Some of these considerations in digital trading environments such as multiplayer online games and e-commerce platforms demonstrate how the implementation of reputation mechanisms, feedback systems, and institutional constraints can influence trust, fraud, and market stability. Previous research in this topic highlights that anonymity, asymmetric information, and low enforcement costs can incentivize opportunistic behaviour from agent and that though this reputation systems can function as informational signals that reduce uncertainty and discourage misconduct. Some insight gained from some studies from gaming economies, online marketplaces, and blockchain-based trading systems suggest that reputation can accelerate the convergence toward cooperative equilibrium, improve price stability, and mitigate fraudulent activity in an economic system however its effectiveness depends on design structure and enforcement credibility within the system. The study builds upon these insights by developing an agent-based computational model in which heterogeneous agents choose whether to commit fraud according to a stochastic decision process and update their behaviour accordingly through payoff-based learning. Through the study two institutional regimes are compared: with the first one being in which reputation affects market allocation and one in which it does not. All other structural parameters, including auditing intensity, productivity distribution, and price adjustment dynamics, are held constant as not to affect the integrity of the experiment. The outcomes of the study are evaluated using 100 Monte Carlo simulations for each regime to ensure statistical reliability through a large enough sample size. The results of this study show that while formal auditing alone eventually suppresses most fraudulent behaviour, the presence of a reputation mechanism significantly accelerates convergence toward a system with a low fraud temperament. Faster fraud reduction stabilizes aggregate supply earlier, leading to lower transitional price levels and reduces the price volatility in the system. Though in the long term the anti-fraud transition appears similar across both regimes, The implementation of reputation materially improves the adjustment dynamics by strengthening the long-term incentives for honest behaviour in the system. These findings suggest that a decentralized reputation system functions as an endogenous enforcement mechanism and that it complements the formal regulations and would enhance the efficiency in a dynamic market.

Introduction

Why do games keep implementing them, why are they so prevalent?

The reputation systems are commonplace in games as a tool to influence player choices and they also provide a scalable way to make game worlds feel reactive to player actions or to allow other players to judge the reliability of others in multiplayer games.

What is the brief, high-level history behind reputation systems?

Historically, reputation systems have been present in a variety of video games evolving from rudimentary binary moral choices in early RPGs to complex and nuanced choices in modern titles and are being used as a tool to curb toxicity in multiplayer experiences.

What does your study hope to achieve / analyse here?

This paper aims to analyse the usage of reputation systems in games and would focus on analysing studies on player behaviour and motivation, the realism and immersion of the game world as affected by the NPC interactions and the effectiveness of the related game mechanics.

How are you doing this analysis?

This study will analyse a variety of papers on the subject before utilising the concepts and methodologies to develop an artefact that will interact with these philosophies and attempt to solve the prevalent issues with the mechanic in modern games

What is their application towards economics?

Reputation systems have many applications in an economic setting being in various marketplace types in the online environment being used in a variety of situations to limit fraud and scams due to the ease of committing criminal action in a digital environment.

Literature Review

Concept of simulated economy is the buyer and seller attempting both to come out of engagement with a positive value gain from the transaction. The reputation system implementation is to affect this dichotomy so that neither party reneges on the deal for further personal short-term gain. This is relevant in all forms of online transactions as in situations such as games or direct marketplaces agents are more willing to hide behind anonymity in order to generate value for themselves even if the method is unethical as there is a smaller chance for retribution.

Existing Systems and their applications

Whilst present in a plethora of game genres, reputation systems have been most popularly implemented in role playing games (RPGs) like World of Warcraft. This paper, 'PlayerRating: A Reputation System for Multiplayer Online Games'[1] discusses how online multiplayer games like use a reputation system called ‘PlayerRating’ to curb anti-social behaviour between players as it “It leverages the prior experiences of a player’s peers to determine the reputability of all other peers, allowing well-behaved players to safely congregate and avoid interaction with antisocial peers”. The paper also explains that the reputation system in World of Warcraft exists to promote positive behaviour. The paper mainly seeks to discuss the player rating system in World of Warcraft where players can rate each other based on their actions with various weighting implementations to make the system more accurate and less susceptible to being manipulated. This is relevant as multiplayer games like World of Warcraft feature their own economies. World of warcrafts economy is a player-driven market mostly centered around a feature called “the Auction House”, where players trade goods for gold. This system is often fluctuation in a similar fashion to a real-world economy being affected by the same sort of things such as supply and demand. The system is also similar to a real-world economy in how its engaged with such as through market speculation and bots.

A second paper that much more thoroughly explores the economic landscape of World of Warcraft is that of “The Value of Currency in World of Warcraft”[2] which details the currency exchange in World of Warcraft as an “in-game currency” which is, according to the paper, most commonly referred to as “gold” and is the highest ranked currency, as opposed to silver and copper. The paper details the currencies, and their three variations: gold, silver and copper. A hundred pieces of copper is the same value as one piece of silver whilst a hundred pieces of silver is equivalent to one piece of gold.

Steam

Like World of warcraft, Steam has its own economy however steam is an online game storefront with a secondary cosmetics market rather than being itself a game with the main markets for cosmetics being supported being CS2 and TF2 both of which were published by steams parent company, valve. The paper “Characteristics of Online Gaming Market Structures: Evidence from Steam’s Online Gaming Marketplace”[3] explains the steam marketplace saying that it connects a plethora of buyers with a large selection of anonymous sellers who price their items with a variety of reasons in mind, such as pre-existing expectations and the observable quantity of the items in circulation as that time. The paper also postulates that all items at one point or another reach a stable equilibrium price. It also believes that the marketplace also diverges from real-world marketplaces due to the incontrovertible fact that the initial value for a large pool of items is artificially created by Valve as they have full control of the amount that is released for sale and can manipulate the market at any given time by releasing more of the item. The paper also posits that by virtue of large trade numbers that “they are likely to have their item sold at a competitive price.” the paper also argues that “social interaction can become more volatile and deceptive” and therefore hypothesises that trading successfully in these such markets requires a pre-existing understanding of an item’s value, its ability to interact with other users, and the access to information that could determine publicly perceived value for any given item. The paper discusses that in the steam system users can collect any item that can be purchased and then place the item for sale in the marketplace at the current market price at the moment of being placed for sale. The paper also has an emphasis on Steam’s item bidding system which it explains as a matching system where a user can place bids on items that may not currently not available and Steam “matches” that requested price with a requested item once it is made available at a minimum quantity and moves the next person in the queue up for the proceeding price requisitioned, once another copy of the item becomes available the next requested price. Steam will then take a prespecified percentage of the item’s final sale price in the form of a transaction fee, in turn having a causatum upon the value reflected in the final listing price. The paper suggest that this presents transaction fees as a cost of trading in the marketplace for the users. The paper compares the price bidding system to a real time auction as it is believes that the concept is consistent with “neoclassical economic theory” and that it suggests that the prices and therefore the scarcity are the biggest determinant factor in the question of the quantity sold and in the amount of a product that is purchased. The paper also delves into the topic of the items themselves and their nature as virtual items saying that in environments such as online gaming marketplaces, the items that are produced and sold are not concrete as they cannot be physically held as they exist purely virtually and are intended purely to affect aspects of a virtual character, they are not created by any labour outside of the virtual environment, and they usually don’t serve a unique purpose or are utilized in a particular situation that is not already fulfilled by the default weapon skin cosmetic. The paper further hypothesises that there is there is no particular supplier of inputs, no cost to the previously mentioned inputs, and almost no costs involved that is Wholey unique to producing an online tradeable item other than the labour by the programmer and possibly an artist.

Another thing the paper explains about the economic system of steam is its anti-bot and anti-cheat safe measure as any given user requires “five dollars”, in America but the price will fluctuate region dependently, to open a Steam account. This paper believes this additional cost will be advanced to the consumers. This therefore creates a situation where there are price constraints before a customer can even participate in the market. The paper also later elaborates on this point by explaining that the strictness is a product of attempting to minify scammers and to disincentivize the high frequency of trades outside of the previously mentioned “Steam Guard” requirements. It also seeks to find an alternative explanation for reduced transactions on the marketplace over time which it argues is caused by “the rise of third-party markets” in which it gives the example of a website marketplace called “OP Skins” along with increasingly restrictive time constraints the Steam market imposes on trade. The paper discusses these third-party markets and their similarity to Steam arguing that they serve as another hub to connect buyers and sellers of various in-game tradable virtual items from different games but explaining that third-party markets have different transactional costs, trade-offs and beneficial features that the Steam. The paper then details the transactional differences between steam and these third-party websites stating that when a user lists their item on the marketplace to be purchased by another user through the available options such as buy order and direct purchase, Steam takes a percentage cut from the item sale. The paper posits that the very minimum, price of the fee would be “two cents” or the equivalent value in other regional currencies. It also posits that in normal circumstances; there is a threshold for the price. If an item listed on the Steam marketplace is sold past a certain price, Steam will take a 15% cut with 10% going towards the publisher and the remaining 5% to Valve, Steams parent company. The paper also acknowledges that minor transactions fees occur in third-party markets as well, but postulates that they are not as oppressive. The paper substantiates this belief by explaining that third-party markets offer “cash out” features, which it believes gives the users greater freedoms to buy and increase the average buyers purchasing power. The paper also hypothesises that this would also increase the buyer's sense of confidence due to the fact that proportionally the price of their items are recoverable and can easily be converted into usable currency within a PayPal account or into a currency that is exclusive to that website.

A second paper that discusses steam; ‘Behavioral Consequences of Value Perception in Steam Community Market Users’[4] which aims to “advances the understanding of the dynamics of C2C markets for virtual goods” which it does through an observational analysis of the primogenitor of loyalty, including the “aesthetic dimension” of perceived value, to achieve this the paper sampled 157 steam users from Brazil.

Overall, this paper details the effects of the steam marketplace, the presence of anti-business practice techniques to improve the trade-to-trade relationship between users. This market chooses to forgo a reputation system by instead having the system be semi-autonomous and as trades in this market are facilitated anonymously and without direct interaction between the seller and buyer there is little opportunity for either party to cheat or steal during the interaction and therefore represents a system that could argue against the need for a reputation system in e-commerce, although the system has its own flaws as Tyler Clark puts it in Characteristics of Online Gaming Market Structures: Evidence from Steam’s Online Gaming Marketplace; as the paper purports that it makes economic sense for a user to undercut competition (i.e., “other users who post listings in the marketplace with some expectation of a transaction”), which it believes would otherwise impede economic growth and decrease profit to zero in an real-world market for a tactile product, this drives the paper to conclude that the foundation of online marketplaces for virtual items is imperfect. The paper believes that this leads to a “rise in third-party market” that attune the demand of items and the available services like “cashing out.” The paper elaborates that the consequences of these trades and transactional events include “artificial price bubbles” within any given virtual marketplace, and predacious market manipulation due to the present incentives for the users to gain a profit and in part due to the eagerness of the user to pay for the associated transactional costs which the paper gives the examples of “time spent to trade or actual money” or precluding additional profits for the convenience provided by 3rd parties

Ebay

Ebay unlike steam and World of Warcraft is not particularly games orientated and is more a general online e commerce store more focused on its draw of being the premiere platform that the general person can sell items on and as such would require a reputation system as the individual is more likely to get away with swindling a buyer than a business which would have to contend with the large public reputation system that is modern society. The paper “Analysing the Economic Efficiency of eBay-like Online Reputation Reporting Mechanisms” [5] details models such as ebay that “rely on binary reputation mechanisms for quality signalling and quality control”. In this model the “sellers keep their actual quality private and choose what quality to advertise. The reputation mechanism is primarily used to determine whether sellers advertise truthfully” the paper posits that “Sellers aims to maximize the present value of their payoff function” which using that fact it therefore concludes that this means “sellers have an incentive to over-advertise quality.” and likens it to the “market for lemons” concept. The paper also suggests that “the more lenient buyers are when rating sellers, the more likely it is that sellers will find it optimal to settle down to steady-state quality levels, as opposed to oscillating between good quality and bad quality”. The paper ends by stating that it is “questionable to what extent unsophisticated buyers are capable of deriving and applying it correctly in actual settings”

Another paper “Sustainable reputations with rating systems” [6]discusses the use of rating and reputation systems in real world economies such as eBay to facilitate an analysis and quantification of the provided service by the seller. The paper mostly angles on how this can be achieved in a sustainable manner due to the fact that providing too harsh sanctions upon either party would result in the system becoming defunct as both parties seek to improve profits with each further transaction. The paper also seeks to demonstrate that “if buyers are lenient enough when they rate and correspondingly strict when they judge seller profiles, sellers will find it optimal to settle down to steady-state true and advertised quality levels if such an equilibrium exists under perfect information.” This papers objective is clearly to explore to what extent “binary reputation mechanisms”, with the one used by eBay as an example, and see if it is capable of inducing efficient market outcomes in marketplaces where the true quality information is unknown to buyers, a second “where advertised quality is completely under the control of the seller“ and a third scenario “where the only information available to buyers is an item’s advertised quality plus the seller’s feedback profile”

The paper suggests that reputation systems are positive, but it also argues that “the value of reputation mechanisms in general relies on the assumption that past behaviour is a reliable predictor of future behaviour”. In order to substantiate the positive position on reputation systems the paper also provides the counterpoint that “buyers make purchase decisions based on knowledge of prices and estimated qualities” and that a reputation system is at the end of the day an estimate of the sellers qualities based on their previous interactions with others.

The paper posits that “in the presence of competitive marketplaces, buyers would then eventually leave the marketplace in favour of other markets with better information”

RuneScape

In comparison to the previously mentioned marketplace; steam, RuneScape possesses two marketplaces one that is run by the company as a unified in-game marketplace and the second is the player-to-player interactable marketplace where people will sit in a commonly travelled location and trade wares with other players. Whilst the latter is more efficient and held up by RuneScape's developers Jagex with this being a recent development, only being around for a few years of RuneScape's multi-decade existence. Marketplaces and trading are a large part of RuneScape's identity as the paper “Learning Economics in the Massively Multiplayer Online World of RuneScape”[7] explains, the initial tutorials a player would encounter in the game focus on teaching players how to make things. The paper believes this is emphasis is crucial due to the fact that the game revolves around earning money which can primarily be achieved through producing and selling goods or services. The paper explains that there are two methods of trade within RuneScape, with the first occurring at a location known as the Grand Exchange, the paper describes it as “a central marketplace where buyers and sellers gather to trade their wares”. The paper details that the Grand Exchange operates very similarly to the likes of a real-world market in which the prices are determined by the transactions of all players involved in the game regardless of exterior factors and following the concept of supply and demand. The data on pricing and the traded numbers are available publicly with this allowing for an easy time studying the data. The grand exchange operates using the concept of supply and demand. Item prices, usually referred to as guide prices are determined by recent transaction volumes and market activity particularly in situations such as high demand/low supply leading to an increase of the prices, and low demand/high supply decreasing them. Another paper “REAL ECONOMICS IN VIRTUAL WORLDS: A MASSIVELY MULTIPLAYER ONLINE GAME CASE STUDY, RUNESCAPE” [8] discusses trading irrespective of the marketplace due to it being written before the marketplace’s integration and as such the effects of a non-centralised trading economy in relations to reputation. The paper details the two main types of trading in the game at the time being that of NPC trades in which trading with non-player characters is usually referred to as PVE, which stands for player vs. environment trade, and player to player trades which the paper refers to as PVP (player versus player) trades. The paper explains that NPC trade takes place either in general stores or in specialty shops. It details that every store has only one or two shopkeepers serve all players at the same time. General stores buy and sell any type of items, whilst specialty shops buy and sell limited types of items. The paper gives the example that, players can purchase swordfish, shrimps, and fishing gear from a shop that specialises in fishing, but not a sword. The paper says that most stores keep two different types of inventories simultaneously, these being a “main stock” and a “player stock”, both of which are contained within different tabs in the interface. The paper explains that the main stock consists of things that would be considered ordinary items with the RuneScape economy, such as pot, jug, and tinderbox according to the paper, which are supplied by the game to the vendors in an unlimited fashion, while player stock only consists of items that are sold to the store directly by the players. The paper posits that due to the fact that the main stock items are provided infinitely, players can always rely on their supply, hence the paper concludes that this is why items in the main stock are generally priced higher than items in the player stock.

The paper also details Player to player trades and explains that this is a section of trade that includes all trading activities that are performed between two players without a mediator. In PvP trade, players exchange virtual items either for gold pieces or for other items. |The paper also details bartering as a type of PVP trading that is an old method of trading, citing that it is no longer efficient in the “monetary world” the paper found itself in at the time it was written, but it proceeds to explain that bartering was very popular in RuneScape, before the introduction of the previously discussed Grand Exchange. The paper says that PvP trade requires more attention in comparison to the NPC trades due to the fact that it is somewhat predatory towards lower experienced individuals as in PvP trades players might end up with a loss if they don’t know the actual market price of that specific item. The paper also explains that Profit is generally high if players are selling an item considered rare and that otherwise players must sell large quantities of items considered more common to make an equal profit. The paper also details how player who desire to practice this form of trading would usually stand at crowded places such as bank courtyards or public squares and shout, “sell strength ammy 2k!” The paper explains that this means the player is selling “an amulet of strength” for “2,000 gold pieces”. The paper next explains that, eventually a buyer would approach, and the seller would see a “player x wishes to trade with you” message on the general messaging box. The paper next says that if the seller wants to facilitate the trade with the other player, they would right click the other player’s avatar and select the "trade" option which would open the trading interface. The paper explains that in this interface, players would see each other’s offers side by side and that players can trade gold pieces vs. goods or goods vs. goods in this trade. The paper also makes the claim that any item is tradable if both parties are happy with the offer. Naturally however this sort of system as previously mentioned can easily result in scams or be utilised by player that wish to trade their in-game possessions for real world money, these such trades however are against the games terms of service and as such as the paper details measures taken by Jagex to limit scams and real money trading in December 2007. The paper explains that one of the solutions was a system called “Balanced trade”. which as the name suggests, the two players that participate in the trade must exchange items that would be considered to be valued similarly with a margin for a price difference. The paper says that initially Jagex announced a “3,000GP” gap between the proposed value of each side for every 15 minutes in the game and that later this difference was increased so that the limit starts at “5,000GP” for all players and increases up to “10,000GP” for free users and “60,000GP” for players that buy the games membership system for every 15 minutes, with this being dependant on the quantity of quests that players have completed. The paper believes that Jagex succeeded as it limited the real money trade, since players who sell virtual items for real money can no longer transfer such items to buyers for nothing in return.

As previously mentioned, the paper also discusses the Grand Exchange as a method of trade and released at a somewhat recent date to the publishing of the paper being was introduced in November 2007 but years previous to the modern day. The paper talks about how the Grand Exchange is a relatively new update to when the paper was published but is extremely influential upon the trading economy. The paper details that it is a central trading system that shares certain characteristics with commodity exchanges and presents similar qualities to an auction house in RuneScape possessing some of the same qualities. The paper explains that it believes the grand exchange is similar to commodity exchange in the sense that there are only goods traded within the system. The paper contrasts this with real world commodity exchanges, as a concept called futures contracts are present within the system of the Grand Exchange. The paper also says that it works as an auction house by matching the bids of buyers and sellers on traded items.

The paper details that the way the system works is that when visiting the Grand Exchange, the players would place their bids on a large selection of virtual item in RuneScape. The paper then points out that the computer system matches the anonymous bids, and the respective players would receive a message to alert the player to the fact that the transaction was completed. The paper also explains that the Grand Exchange serves players 24/7, and as the paper says does this “regardless of players’ presence in the game, on the same server or even in the GE location”. The paper next details that after placing a bid, players can do any other activity in the game whilst they wait and that most GE orders are completed almost immediately; though this does come with the caveat that some players may have to wait a substantial amount of time for the buy or sell orders to be completed dependant on the items.

The paper also has a large section detailing the agents and compares RuneScape's economy to that of a real-life economy. The paper discusses the concept of “scarcity,” defining it as finding a balance point between limited resources and unlimited human needs. The paper discusses the resources and how it refers to the money, time, and skills for an individual, it also considers capital, the natural resources, and the available labour for the more sizeable economic agents which the paper gives the examples of companies or countries. The paper posits that since the resources in the real world are limited, the existing economic agents are forced into making decisions in regard to their allocation. For this the paper gives the example of individuals that are under their income conditions and how they must choose between paying the rent and purchasing an expensive cell phone. The paper talks further about Jagex and their economical position, being a game company, Jagex, is one of the biggest agents in the virtual economy or the government. The paper also gives an anecdote about how before 2007, the in-game government pursued a relatively liberal approach in the RuneScape economy. The paper believes that apart from the essential decisions that are required to run the game, the existence of the government was almost invisible. The paper also says that players seemed to be the primary economic agents who were evaluating their possibilities and constrains within the economy with the goal to maximize their virtual wealth. The paper thinks that they abundantly determined the item prices in the market, earned high profits from sales, and donated to the other players. The paper also states that many players suffered from the poor economic decisions they made, which is a conclusion it came to based on the limited available information about the market. The economic choices were mostly taken by observing other players for a short time. Since each game server maintained a micro economy, players would never know conditions in the other servers, unless they visited all of them, which was considerably time-consuming, however, some players, according to the paper “called merchant clans”, turned these flaws into extra generated revenue by performing successful examples of “arbitrage” (buying from low price and selling from high price for profit) and drove the market in the virtual world.

The paper discusses the removal of the unbalanced trade, the applications of the trade limits, and the introduction of the Grand Exchange (GE) and how its implementation produced incurred positive and negative implications for the game. The paper believes that it commonly created a more transparent economy where the individual agents have greater ability to understand and appraise the economic conditions of RuneScape and improving the decision-making for all. The paper details that in the modern day of the paper, players can go online and analyse the current and documented historical prices of any item and can the proceed to login to the game and make transactions based upon the information. However, the paper also states that the implementation of new rules also limited so individual agents' capacity to act in such a position. The paper points out that many players protested the implementation of trade limits and the “balanced trade”, but the games government body ignored the outcry in order to protect the welfare of the general community, with the biggest group effected being players in a system called “merchant clans”. The paper describes a merchant clan as a group of players who work for the economic benefit for their members. They claim that players accumulate greater wealth in a short time by joining a merchant clan, as opposed to engaging in individual mercantile activities. The paper elucidates that large merchant clans usually have ability to manipulate market prices and that the implementation of the GE increases the transparency of the market with the daily data feeds and visual graphics limiting the ability for individual agents to successfully scam other agents.

Fraud

Fraud is a large issue in any economy and a leading reason for the implementation of a reputation system, that is to say it's a system designed to prevent repeat actions in the vein of fraud and disincentivises agents from engaging it without preventing it wholesale the first paper “Detecting fraud in online games of chance and lotteries”[9] states that fraud detection is an important topic of research in data mining communities for multiple decades and that various levels of supervised approaches to fraud detection have been proposed for various industries. The paper aims to describe a novel hybrid system for detecting fraud in the highly growing lotteries and online games of chance sector. The author also states that while the objectives of fraudsters in this sector aren't unique, scam scenarios are much more prevalent in these sectors than previously studied ones. There are many situations in which fraud can occur with one of the most common is in that of a lottery in which there is a large variety of ways for any agent to cheat with a common one to be changing values in their personal output in a way to increase their financial gain, be it through weighted die or directly changing numbers. The paper believes that the lack of sorted data for the supervised design classifications, the anonymity of users and the extent of the collated datasets are the other key factors the paper believes are differentiating the problem from previous studies. The paper also thinks there are the primary drivers behind the design and implementation blueprint for the described system. The system in question employs online algorithms that in an optimal scenario would collect statistical information from the collated raw data and applies pre-selected checks against known fraud strategies as well as “novel clustering-based algorithms for outlier detection” which are then combined to produce alerts with high detection success rates at an acceptable level of false alarms according to the paper. Some things that might get false flagged in this scenario include unusually lucky rolls in lotteries or transactions that involve large sums of money due to the fact that these are more likely to occur in a situation regarding fraud than otherwise but them occurring to begin with is not a guaranteed indictment of fraud happening in that situation.

The paper states that cyber-crime has been a constant adversary for all manner of organisations since the beginning of the commercial internet. The paper details that , several approaches to counter-measure cyber-criminal attacks have been proposed in response from various groups and organisations: more powerful authentication and other techniques from the computer and communications security communities aimed at denying falsifying or stealing identities, client or server alike, while intrusion detection and fraud detection techniques aimed at detecting changes from “normal profile behaviour”, or equivalently, at detecting “anomalous behaviour”. Normal profile behaviour refers to the expected or typical pattern of actions exhibited by an agent under ordinary, non-conforming conditions. Anomalous behaviour on the other hand refers to the statistically unusual or structurally inconsistent actions relative to the behaviour of the previously mentioned normal profile. For anomaly or outlier detection, a wide range of traditional techniques from the machine learning and data mining literature have been proposed, including supervised learning approaches where a set of training data is provided that contains labelled “normal” and “fraudulent” transactions

This paper however does not propose the implementation of a reputation system as a solution to the issue of fraud but does acknowledge that it is a concept that can be used primarily in online games to curb the issue of fraud.

Minecraft fraud

One of the platforms that can facilitate fraud unwillingly is that of Minecraft and the paper “Gamifying Electronic Trading Through a Minecraft Commodities Exchange” [10] discusses this. The paper explores this through a survey of previously known security vulnerabilities in Massively Multiplayer Online Games such as Minecraft and describes how these are utilised by malicious agents to cheat. The authors state that while such abuse often with the aim to gain an edge in the game, that there is a recent trend of financial fraud in such games. they review the common types of online fraud, which it gives the examples of phishing and click-fraud that the paper believes will increasingly migrate into the online sphere in games such as Minecraft. The paper refers to the resulting abuse as virtual fraud. By defining a visual classification of virtual fraud, the paper aims to lay a foundation to future investigations of the problem. They also use a visual classification to describe various types of virtual fraud that the paper believes may become particularly threatening.

Given the significant role that exchanges play in the global economy, integrating similar mechanisms within a virtual environment like Minecraft can serve as an engaging gameplay feature and a powerful educational tool. By simulating real-world trading and market dynamics within the game, players can gain a deeper understanding of economic principles and financial markets in an interactive and accessible way.

The paper presents the design and implementation of a virtual commodities exchange within the game Minecraft, and how the transforming of in-game items into tradable digital assets replicates key features of real financial markets. The authors integrate a dynamic electronic trading system into Minecraft using a custom mod/plugin, including a limit order book, market-making algorithms, and a player-driven market governed by supply and demand. Players would interact with the exchange by placing buy and sell orders for virtual goods similar to RuneScape in the previous section, allowing the in-game economy to develop organically and offering an interactive environment that would mirror real market dynamics. The observations of player behaviour in the paper revealed that the users quickly adapted to the system and even exploited initial inefficiencies in pricing, demonstrating a capability for authentic economic decision-making within the game’s virtual environment. The platform’s operation illustrates how complex financial principles such as the mechanisms for pricing, the market depth, and strategic trading could be gamified and made accessible for educational purposes in a risk-free setting.

Economic considerations

A paper, “An evolutionary game model with reputation threshold and reputation score to promote trust in the sharing economy” presents an “evolutionary trust game model” that sets a reputational threshold and also chooses to implements a reward system for participants whose individual reputation scores are above this threshold; conversely, a punishment mechanism is applied to those whose scores are below it, to investigate the formation of trust in the sharing economy” The paper aims to present the dynamic evolution of four select types of participants and how the reputation meter increases throughout 5 scenarios. The paper also provides heat maps of a purported 10,000 participants and their evolution of both the reputation scores and utilised strategies “over time steps when the reputation threshold is low, moderate, and high”. In This paper, “Economic Design of Reputation Systems” [11]details the economic forces behind the implementation and their application in real market scenarios. it also seeks to identify the key attributes present, such as the users trust and the rate of the contributions that control the actions of users of various trading systems irrespective of whether or not they are cooperative, or display selfish, or malicious tendencies. and the paper further studies this through creating an economic model that captures the behaviour of the peers in a system that employs various incentives and reputation schemes to mitigate the preexisting effects of “freeriding” and the misbehaving actions of some of the agents. This is all presented with the stated aim of furthering insight into the subject and a further understanding of the operations and maintenance of the reputation system.

This paper, “The Economics of Reputation and Feedback Systems in E-Commerce Marketplaces” [12] studies e-commerce and how reputation systems can affect them through discussing various feedback systems in e-commerce and their economic impact. This paper gives an explanation for why reputation matters from an economic perspective through explaining how trust decreases the agent's uncertainty around purchases and is a proxy for their future behaviours. This concept explains how agent decisions could depend on reputation within the simulation and it justifies why agents would change their behaviour based on other agents past actions, choosing to cooperate with higher-reputation agents. Another thing this paper suggests would be to incorporate concepts that would be negative but exist in a real world scenario like asymmetric information which is the concept that can cause market failureas one party in a transaction has more or better information than the other leading to a party choosing to act in only their own interest and compromising the transaction. Tadelis explains how the implementation of a reputation system could limit or prevent the effects of the aforementioned, asymmetric information by constituting past outcomes into an indication of possible future behaviour. These ideas can be utilised to justify features and design choices, such as tracking past interactions, scoring agents, and the effect reputation has on future trade or cooperation decisions.

Implementations

https://jasonfantl.com/posts/Simulated-Economy-(2)/

There are many ways to implement a reputation system and to do so one requires to simulate an economy, one that stands out as particularly detailed is Jason Fantl and his series of blog posts about coding a simulated economy [13]. The author chooses to begin with a single market, where each actor will keep track of their personal value of a good and the price, they expect to pay for the product. The blog states that from that point you can tell if they are a buyer or seller: which it defines as a buyer being an agent that personally values a good more then they expect it to cost and that a seller is an agent that values a good less than what they expect it to cost in the market.

The author mentions that as it's a starting point the first form of the simulation should be as simple as possible, with no money is given in a trade, no limited quantities of goods, no transactional costs, no diminishing returns, with there only being transaction offers. The blog states that they will attempt to buy and sell with each other at random and that in order to have a convergence of prices, the buyers would have to decrease their expected price after a transaction, and sellers would in contrast increase their prices. The opposite should be implemented to happens on a failed transaction as the buyer would learn from the experience this would be further improved with the implementation of the reputation system. The paper then explains that with the current implementation suggested by the paper the market would applies forces that try and balance the number of buyers and sellers, penalizing those who don’t get matched up. with this being relevant to the considerations of the supply demand curves.

The blog goes into further detail of extra implementations however these possess very little value in the context of the implementation of a reputation system.

There are multiple methods of implementing a reputation system each with their own positives and negatives. The first one and most commonly used is that of a rating system where any given agent can input a score

Blockchain-Based Reputation

Another paper “RBT: A distributed reputation system for blockchain-based peer-to-peer energy trading with fairness consideration” [14] details that its implementation relies on the blockchain, which it specifies “smart contract technology”, to achieve distributed and automatic management of reputation. The paper details how this distributed reputation system helps to implement a consensus algorithm for blockchain and a “reputation-based 𝑘-double auction matchmaking scheme” for peer-to-peer energy trading.

In addition, the paper defines an indicator of fairness as to capture the reputation-based average benefits and costs when considering reputation contributions in a peer-to-peer energy trading market. The paper states that when simulating the extensive system, the numerical results demonstrate the effects of distributed reputation in improving the efficiency of blockchain and balancing fairness indicators between sellers and buyers during peer-to-peer energy trading.

Feedback-Based (Rating Systems)

Feedback is the most common variation of reputation systems in online environments with a particular presence in e-commerce being the system used by most of the marketplaces mentioned earlier in the literature review, particularly ebay and steam. This is a system that is a mechanism in which agent’s past behaviour is recorded and integrated into a publicly observable score that influences future economic opportunities for the agents. Systems such as these operate through collecting evaluations which are either explicit ratings or implicit performance signals from previous transactions and updating the agent’s reputation accordingly. In markets characterized by such information, the presence of a feedback-based reputation serves as a signalling device that reduces uncertainty about counterpart reliability which it does through linking historical conduct to future market access, it creates intertemporal incentives: agents who behave honestly accumulate reputational capital and secure greater market share, while those who engage in opportunistic behaviour face reputational penalties that reduce future income. Unlike purely exogenous enforcement mechanisms, feedback-based systems function endogenously, as discipline arises from decentralized information sharing rather than solely from formal regulation. Their effectiveness depends on factors such as information accuracy, update frequency, resistance to manipulation, and the credibility of penalties, all of which determine whether reputation meaningfully alters long-run incentives.

Weighted Reputation Models

A paper, “Bayesian Reputation Systems” [15] discusses both weighted systems and compares it to Bayesian reputation implementations. The paper details that the most common approach to computing the reputation score in commercial systems is to use some form of weighted mean, which is to say some form of computation method based on weight distributed around the median rating which can provide more stable reputation scores than scores based on the simple mean. The paper also explains that it is also possible to compute scores based on fuzzy logic implementations. The paper also states that user-trust and time-related factors can be incorporated into any of the reputational computation methods.

Bayesian Reputation Systems

The previously mentioned paper “Bayesian Reputation Systems” [15] obviously also details Bayesian reputation systems which it explains that this form of reputation system uses probability theory to calculate an agent’s trustworthiness by continuously updating their reputation based on new ratings. Using methods like Beta distributions for binary good or bad and Dirichlet distributions for multi-level ratings, these systems collate previous reputations with additional evidence to estimate the probability of future positive performances.

Behaviour-Based (Implicit Reputation)

This refers to the unconscious, automatic, and uncontrollable attitudes, stereotypes, or associations that could influence an agent's behaviour and their judgment toward other agents. Unlike explicit reputation, which is based on conscious beliefs, implicit reputation is formed through experiences and consumed media, furthermore it can exist even when an agent explicitly rejects perceived prejudices. Ostensibly this type of reputation system is just the opinions of agents based on prior experiences rather than any specific implementation.

There are more methods of implementing reputation systems than stated above however these serve as a selection of the possibilities going into the methodology for the project.

Methodology

What implementation was used in the artefact?

The artefact was made using a continuous score-based reputation system, of which is a mechanism for evaluating the trustworthiness, reliability, or performance of agents by assigning them a dynamic, numerical score that updates in real-time based on cumulatively assessed behaviour. Ostensibly

How to design reputation scores

The implementation of reputation is predicated upon the scores for each agent in the simulation. This is achieved in the simulation through a bounded score between 0.0 and 1.0 that evolves each turn based on productivity and decay. The reputation is tied purely to each agent's productivity and performance and therefore is relative to a fixed benchmark which in the artefact is 1.0. The artefact also uses alpha and delta as pre-defined variables to limiting the speed at which any agent’s reputation can be affected in the simulation, with alpha equalling 0.05 which equates to only 5% of the performance gap effecting reputation per turn. This is done to make the adjustments in reputation gradual, sustainable, and reflect long-term trends rather than short-term volatility. This is implemented in the program to create a more realistic and manageable simulation. Delta on the other hand is calculated through the value of what is produced minus the expected output then the whole sum is divided by the expected output, this is essentially a productivity growth rate relative to a benchmark. Both of these concepts, alpha and delta, are extremely important to the implementation of reputation in the artefact as they essentially correspond to reputation yields. This is due to delta existing as a formula to calculate an agent's total return and Alpha being a market reaction coefficient, with these two values reputations can calculate reputation yields based upon the market effects and returns. Another important implementation towards the simulation of reputation is the reputational decay as without it the reputation system can easily be gamed by agents as overperforming early locks in high reputation forever and even if performance later drops, the agent would face minimal consequences for their actions. This would cause the system becomes path-dependent and rigid. The implementation of decay in the artefact is set so that every turn each agent has their reputation decreased by 1%. There are other important reasons for the implementation of decay such that agents must consistently perform well to maintain reputation and that if they only meet the minimum expectations their reputation will slowly decrease over time. Another detail related to this implementation is the imposed limits, as mentioned at the beginning of the section the score is bounded between 0.0 and 1.0, as such decreases of the score can never be so severe the agent goes into negative reputation and in the opposite regard an agent can’t be so perfect that their reputation never exceeds a perfect score of 1.0

The implementation of fraud in this system is predicated upon the previously explained system, fraud does not directly increase reputation; it will only affect reputation in conjunction with an audit, which has a chance to catch the agent. if the agent is caught it results in a severe reputation loss of 80%, as such in this system the downside for getting caught is severe and doesn't have any benefit unless they pass the audit which is unlikely. Although agents committing don't gain actual reputation until after they pass the audit fraudsters temporarily appear 50% more reputable when allocating demand.

Overall, the features implemented in the artefact essentially create a reinforcement-style trust economy with regulatory risk.

Research Design

This study employs an agent-based Monte Carlo simulation to examine whether the inclusion of a reputation mechanism would improve market stability relative to a similar system without reputation implemented. The study models a decentralized market simulation composed of amalgamate agents who produce, trade, and make probabilistic decisions regarding disincentivised behaviour, with fraud being the main implementation of such a concept in this model. This study compares two institutional regimes, those being a reputation regime, which is a market allocation dependent upon the reputation of the agents and a non-reputational regime being the opposite of the previous regime and the market allocation being independent of any reputation. All other structural parameters are maintained as constants across both regimes to isolate the effect of reputation during the study.

Agent Structure

The simulated economy used in the study consists of 100 agents operating over 200 discrete time periods. Each individual agent has multiple charactering factors, with each agent possessing money holdings, their productivity which is decided randomly at the point of initialisation, reputation, their tendency for fraud and the decision making regarding the fraud

Productivity in this model is time-invariant and drawn once at initialization from a uniform distribution, which introduces a form of structural heterogeneity into the productive capacity of all agents. The initial fraud tendencies are also drawn from a uniform distribution, generating variation in baseline behavioural preferences of the agents. Reputation and money holdings evolve internally throughout the simulation based on the presented market outcomes, audit penalties, and learning dynamics, this initialization ensures that the economic outcomes emerge from decentralized interactions among the agents with diverse characteristics rather than from a collective representative behaviour.

Fraud Decision Process

Once every turn, agents decide whether to engage in fraudulent behaviour according to a Bernoulli process. Specifically, the probability that any given agent decides to commit fraud. The chance they decide to engage with the fraud action is equal to the agent’s current fraud tendency parameter. This ensures that fraudulent behaviour is stochastic rather than deterministic and due to the fact that fraud tendencies evolve over time through the learning dynamics, fraud behaviour is both probabilistic and derived internally from the system.

Production and Effective Supply

in the model each agent produces an output proportional to their individual productivity parameter, which is decided at initialization this however can be modified through fraudulent behaviour which will reduces the agent's effective output. If the agent behaves honestly however their effective productivity will be equal to the systems baseline productivity. To modulate this if an agent decides to commit fraud and is caught, their effective productivity is reduced to 70 percent of the baseline productivity as a penalty. The cumulative supply is defined as the sum of effective productivity across all agents, these aggregate demands are presumed to be fixed and to equal the number of agents in the simulation. This causes price dynamics to be driven by variations in the cumulative supply that would be affected by agent’s fraudulent behaviour.

Price Formation

The price develops regarding the excess demand in the market, the excess demand is defined as the difference between the aggregate demand and the aggregated supply, normalized by the previously mentioned aggregate supply.

Another factor in this is the price updating rule which specifies that the next period’s price is equal to the current price multiplied by one alongside the addition of the price adjustment parameter time’s excess demand. The price adjustment parameter is set equal to 0.1, This whole formula exists to ensure that the price rises when the supply falls below the demand and will decrease appropriately when supply exceeds demand, obviously this is a simulated form of supply and demand. Consequently, to all of this, fraud somewhat indirectly affects prices by reducing the available supply.

Market Allocation Mechanism

The allocation of market share differs between the two implementations, in the regime with reputation present, market share is proportional to the reputation of the agents. Specifically, each agent’s share of total demand is equal to their reputation divided by the sum of reputations across all agents. In this simulation the higher-reputation agents receive a larger portion of market demand. Fraudulent agents may temporarily benefit from reputation weighting, but the audits reduce their reputation and consequently the agent’s future income. In contrast, under the regime without reputation, the market share is distributed uniformly across all agents. Each agent receives an equal fraction of the total demand, equal to one divided by the number of agents. as such obviously reputation affects income distribution and behavioural incentives only in the simulation that includes reputation.

Reputation Updating

Reputation evolves dynamically based on relative performance. During each turn, an agent’s reputation is updated in relation to their productivity relative to the expected productivity benchmark. Reputation increases when productivity exceeds the benchmark and will otherwise decrease. The updating rule incorporates both a learning parameter and a decay parameter, thus ensuring that the reputational changes are gradual and as mentioned in previous sections bounded. The reputational values are constrained to lie within the closed intervals; this dynamic mechanism allows reputation to serve as a persistent but adjustable indicator of an agent's previous performance.

Auditing and Penalties

In the model fraudulent agents are subject to probabilistic audits, each fraudulent agent faces a fixed probability of audit equal to 0.05 at any given time. If an agent is audited while in the act of committing fraud, two penalties are imposed. Firstly, the agent’s reputation is reduced by 80 percent, substantially lowering the future market share of the agent in the regime using reputation. The second penalty is that the agent’s monetary holdings are reduced by 10 percent, representing a financial fine. This mechanism is introduced to mimic formal enforcement in the system and creates an economic deterrent to fraud for the agents.

Learning Dynamics

The agents are designed to adapt their fraudulent tendencies over time based on the realised payoffs, if the fraudulent behaviour yields positive payoffs for the agent, they will increase their fraud tendency by a proportional factor to the payoff, scaled by the learning parameter. Otherwise, if fraud yields a negative payoff for the agent, the fraud tendency will decrease proportionally to the magnitude of the loss, scaled by a regret parameter. These Fraud tendencies are bounded within the interval, ensuring that the probabilities will remain well-defined throughout the simulation. This adaptive rule introduces behavioural learning and a path dependency into the model, as each past outcomes affecting agents will influence their future decisions.

Monte Carlo Structure

As the model incorporates stochastic elements such as including fraud decisions, realization during an audit and heterogeneous initial conditions, as such a single simulation is insufficient to characterise any expected systematic behaviour. To combat this, the study employs a Monte Carlo design consisting of two independent simulations that run for each monitored institutional regime. Each of these runs use a distinct and random seeds, ensuring a complete statistical independency across multiple trajectories. The aggregate outcomes are computed as an average across all the runs. For any variable the reported estimate equals the sample mean across simulations. By the Law of Large Numbers, this estimator converges to the expected value of the stochastic process as the number of runs increases. This approach allows inference about any expected economic outcomes rather than relying on a singular stochastic realization.

Outcome Measures

The model has multiple primary outcome measures which include the average fraud rate over time, the price trajectory, price volatility, and the convergence speed of fraud. The central comparison of these evaluates the expected price path under the simulation with reputation relative to the expected price path under the no-reputation simulation; in doing such this comparison isolates the economic impact of the implemented reputation mechanism.

Identification Strategy

Causal identification is achieved in this model by holding all structural parameters constant across regimes while varying only the presence of reputation in the market allocation rule. Furthermore, both regimes are evaluated using the same Monte Carlo structure and utilise comparable random seed sequences. As a consequence of this any systematic differences in observed outcomes can be attributed purely to presence or absence of reputation rather than to any underlying random variation.

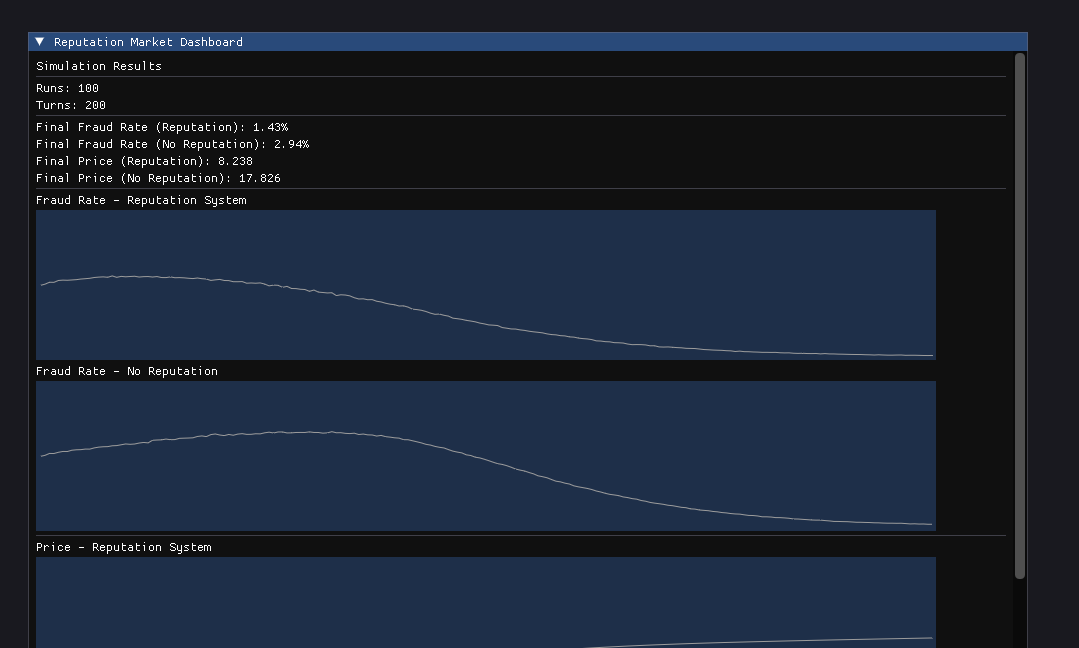

Results Overview

This section presents the comparative outcomes of the two regimes, comparing the presence or lack thereof of reputation. All reported values represent Monte Carlo averages over independent simulation runs and the reported time-series figures display the mean across the runs.

Fraud Dynamics

Figure 1 presents the average fraud rate over time under both institutional regimes.

In both simulations, the rate of fraud declines over time due to adaptive learning and audit penalties. However, the rate of decline differs substantially, and the decline is systematically faster under the Reputation regime. In early periods, the fraud rate under No-Reputation remains elevated, this is reflecting weaker incentives for honest behaviour in system that doesn’t punish bad actors long term. In contrast to this, the Reputation regime exhibits a steeper downward slope in the fraud curve, presenting a stronger behavioural correction when the behavioural incentive is present. The gap between regimes is largest during the transitional phase, after which both proceed to converge toward the near eradication of fraud. This divergence on the graph serves to confirm that the implementation of reputation primarily affects adjustment speed of the model rather than long-run equilibrium. While any implementation of formal auditing alone eventually suppresses fraud, reputation accelerates this process by reducing the expected long-term payoff from dishonest behaviour which would have positive effects on the generated money.

Price Dynamics

Figure 2 presents the average price trajectory under both regimes.

Consistent with the model structure, fraud reduces effective productivity and causes supply shortages which in turn generating upward pressure on prices. Consistent with the dynamics of fraud, the No-Reputation simulation exhibits higher prices during early and intermediate periods. Price increases are more pronounced and persist longer in the absence of reputation. In contrast, the reputation regime suppresses fraud more rapidly and as such it produces a higher total supply, thus the prices remain lower. Although the price levels converge as the presence of fraud approaches zero in both systems, the transitional price differ and as such are clearly displayed in the graph. This indicates that the institutional design affects the economic adjustment even when the initial implementations are the same.

Price Volatility

Figure 2 also reveals differences in price volatility. The No-Reputation regime displays larger movements during the adjustment period, with this reflecting the prolonged fluctuations in the supply with issues being caused by the presence of fraud. In the Reputation regime however, a smoother convergence is demonstrated. This suggests that reputation not only reduces the duration of elevated fraud but also decrease the economic instability. By accelerating the behavioural stabilization, the implementation of reputation reduces the degree of price swings generated by random fraud decisions.

Summary

Across the 100 Monte Carlo simulations performed for each regime, the presence of a reputation mechanics materially alters the transitional market dynamics. Fraud declines over time in both regimes due to the implementation of learning and that of regular audits; however, the convergence is significantly faster when reputation affects the market allocation as under the reputation regime, the fraudulent agents experience reputational penalties that reduce their future market share, therefore lowering the payoff from dishonesty. As a result, agents will limit their fraud tendencies more rapidly than in the regime without reputation, as in such a system reputation carries no economic consequence. The convergence time, which is defined as the first period in which the fraud rate falls to near zero is consistently shorter with reputation, indicating that the implementation serves to improve the institutional efficiency. Although in the long term both regimes tend toward low fraud levels, the primary difference lies in the speed and stability of the adjustment period.

These behavioural differences generate distinct economic outcomes because fraud reduces effective productivity, and with higher fraud rates the aggregate supply decreases. When the total supply falls below the total demand, the excess demand becomes a positive, leading to rising prices under the model’s price adjustment rule. In the No-Reputation regime on the other hand, faces prolonged fraud which reduces effective supply in the long term, resulting in higher and more volatile prices. As the Reputation regime suppresses fraud earlier it can stabilize the supply quicker and therefore produces lower average prices and smoother price trajectories during the adjustment phase. Overall, the results in the figures indicate that the reputation improves the dynamic market efficiency by limiting the supply disruptions and accelerating stabilization, even though both models will eventually converge at a point of minimal fraud.

Conclusion

The existing literature previously discussed in this paper widely supports the view that reputation systems improve trust and efficiency in online marketplaces. The aforementioned studies of platforms such as eBay, multiplayer game economies, and blockchain-based trading systems argue that reputation reduces asymmetric information, disciplines the opportunistic behaviour that the agents might exhibit, and promotes a cooperative equilibrium, however much of this work relies either on empirical analysis of platform specific implementations or on the stylized theoretical models that create stable behavioural feedback. These approaches present often struggle to isolate the causal mechanisms, as the implementations of reputation systems coexist with other controls such as the transaction fees, platform governance, identity verification, and automated matching systems. This study addresses this limitation by isolating the institutional effect of reputation within a controlled agent-based framework and that by holding the auditing intensity, learning parameters, and market structure constants the simulation identifies how implementations of reputation alter behavioural incentives and macroeconomic adjustment dynamics. The results primarily suggest that reputation improves transitional efficiency and accelerates the fraud reduction and stabilises prices rather than fundamentally changing the long-term persistence. This nuance is often understated in the literature, which tends to frame reputation as a necessary condition for market functionality. Instead, the findings indicate that while formal enforcement mechanisms can eventually suppress the agent’s misconduct, reputation enhances the dynamic stability and speeds of convergence in the model and in doing so, the study contributes a clearer causal perspective to debates on the economic role of reputation in decentralized systems.

There are many scenarios that exist in the modern landscape and a variety of possible implementations of reputation to prevent scams and fraud from occurring. This study has employed a Monte Carlo agent-based simulation to examine the economic effects that would occur when applying a reputation mechanism to a decentralized market with adaptive agents. By comparing a Reputation regime to a structurally identical No-Reputation regime, the study was able to isolate the effects reputation would have in shaping fraud dynamics, market stability, and price outcomes in a system. The results from this study demonstrate that the implementation of reputation functions as an enforcement mechanism and that although both regimes ultimately converge toward low levels of fraud due to audit penalties and adaptive learning, the usage of reputation significantly accelerates the convergence. The decline in fraud also happens more rapidly when reputation implementation is present to influence the market allocation, as the agents will internalize the income penalties incurred through reputational damage in the long-term. In contrast to this, in the model without reputation present the issue of fraud persists over a longer transitional period before reaching a point of stabilization. Due to the fact that fraudulent behaviour reduces the effective productivity of agents, the differences in the fraud dynamics translate into economic effects. The reputation regime exhibits stabilization earlier of aggregate supply and correspondingly lower or less volatile prices during adjustment phases. These findings suggest that the reputation improves dynamic efficiency even when in the long term, both models appear similar across institutional settings. The methodology for this simulation is the Monte Carlo structure as it strengthens the possible inference by averaging across separate random distribution realisations, thus ensuring that the reported outcomes will reflect the expected behaviour from the system rather than from single-path randomness, through all of the structural parameters remain as constants and varying only the market allocation rule, the analysis achieves clear identification of the underlying characteristics. The study’s findings contribute to the broader literature on the informal enforcement mechanisms and market design by demonstrating how decentralized reputation systems can complement formal auditing structures and that even in the presence of regulatory administration, the presence of reputation enhances the incentives for honest behaviour and accelerates stabilization amongst the agents. Although the paper serves the broader literature on the topic as explained previously, there are also several limitations remaining in this implementation of reputation systems. The model assumes that the demand is fixed and as such it simplifies the price formation and the audit probabilities. Future research could be performed to explore the endogenous demand, heterogeneous enforcement intensity, network-based reputation transmission, or strategic collusion among agents which was completely ignored during this study. Additionally, extending the model to continuous-time dynamics or incorporating risk preferences could provide further insights into this topic. In summary, the simulation results indicate that implementations of reputation improve transitional market stability by suppressing fraud more rapidly than systems without it and as such it stabilises supply-driven price fluctuations in the market. Whilst in the long-term fraud may converge under both regimes, the reputation implementations materially affect the path and transitional period through which markets reach a state of equilibrium. These findings serve to underscore the economic importance of reputational mechanisms in any decentralized system.

Bibliography

[1]E. Kaiser and W. Feng, 2009 8th Annual Workshop on Network and Systems Support for Games. IEEE, 2009.

[2]J. Holm and E. Mäkinen, “The Value of Currency in World of Warcraft,” Journal of Internet Social Networking and Virtual Communities, vol. 2018, pp. 1–13, Jun. 2018, doi: 10.5171/2018.672253.

[3]T. Clark, “Characteristics of Online Gaming Market Structures: Evidence from Steam’s Online Gaming Marketplace.”

[4]F. Barros et al., “Data for Behavioral Consequences of Perceived Value Among Users in the Steam Community Market, published by BAR-Brazilian Administration Review,” Adm. Rev, vol. 21, p. 240131, 2024, doi: 10.17632/b5cp8smyfx.1.

[5]C. Dellarocas, “Analyzing the economic efficiency of eBay-like online reputation reporting mechanisms,” in Proceedings of the ACM Conference on Electronic Commerce, Association for Computing Machinery (ACM), 2001, pp. 171–179. doi: 10.1145/501158.501177.

[6]M. Ekmekci, “Sustainable reputations with rating systems,” J. Econ. Theory, vol. 146, no. 2, pp. 479–503, Mar. 2011, doi: 10.1016/j.jet.2010.02.015.

[7]T. Somerville and B. O’roark, “Learning Economics in the Massively Multiplayer Online World of RuneScape.”

[8]T. E. Bilir, “Real Economics in Virtual Worlds: A Massively Multiplayer Online Game Case Study: Runescape,” SSRN Electronic Journal, 2009, doi: 10.2139/ssrn.1655084.

[9]I. T. Christou, M. Bakopoulos, T. Dimitriou, E. Amolochitis, S. Tsekeridou, and C. Dimitriadis, “Detecting fraud in online games of chance and lotteries,” Expert Syst. Appl., vol. 38, no. 10, pp. 13158–13169, Sep. 2011, doi: 10.1016/j.eswa.2011.04.124.

[10]A. Pacini and L. M. Fernando Arruda, “Gamifying Electronic Trading Through a Minecraft Commodities Exchange; Gamifying Electronic Trading Through a Minecraft Commodities Exchange.” doi: XXXXXXX.XXXXXXX.

[11]S. Marti and H. Garcia-Molina, “Economic Design of Reputation Systems.”

[12]S. Tadelis, “The Economics of Reputation and Feedback Systems in E-Commerce Marketplaces,” 2016. [Online]. Available: www.computer.org/internet/

[13]J. Fantl, “Simulated-Economy-(1),” vol. 1, 2023.

[14]T. Wang, J. Guo, S. Ai, and J. Cao, “RBT: A distributed reputation system for blockchain-based peer-to-peer energy trading with fairness consideration,” Appl. Energy, vol. 295, Aug. 2021, doi: 10.1016/j.apenergy.2021.117056.

[15]A. Jøsang, “Bayesian Reputation Systems,” 2016, pp. 289–302. doi: 10.1007/978-3-319-42337-1_16.

BACK TO WORKS